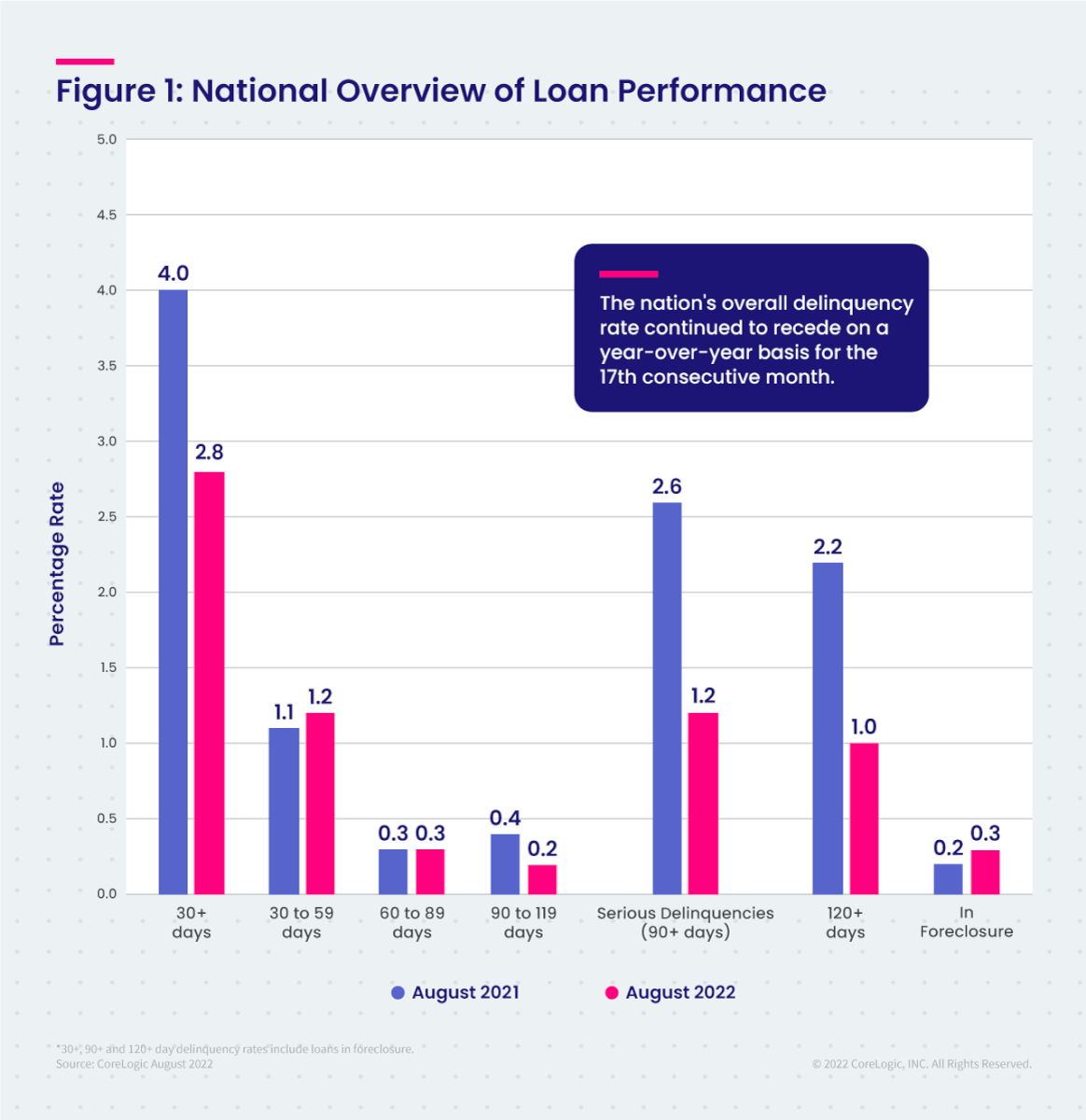

For the month of August, 2.8% of all mortgages in the U.S. were in some stage of delinquency (30 days or more past due, including those in foreclosure), representing a 1.2 percentage point decrease compared to 4% in August 2021.

To gain a complete view of the mortgage market and loan performance health, CoreLogic examines all stages of delinquency. In August 2022, the U.S. delinquency and transition rates, and their year-over-year changes, were as follows:

- Early-Stage Delinquencies (30 to 59 days past due): 1.2%, up from 1.1% in August 2021.

- Adverse Delinquency (60 to 89 days past due): 0.3%, unchanged from August 2021.

- Serious Delinquency (90 days or more past due, including loans in foreclosure): 1.2%, down from 2.6% in August 2021 and a high of 4.3% in August 2020.

- Foreclosure Inventory Rate (the share of mortgages in some stage of the foreclosure process): 0.3%, up from 0.2% in August 2021.

- Transition Rate (the share of mortgages that transitioned from current to 30 days past due): 0.6%, unchanged from August 2021.

The number of borrowers classified as seriously delinquent (90 or more days late) on their mortgage payments in August dropped to the lowest level recorded since April 2020, while the overall delinquency rate remained near a record low. The U.S. unemployment rate has stayed below 4% since the beginning of 2022, and the still-healthy job market continues to help homeowners with a mortgage make payments on time. However, as the cost of basic necessities mounts with rising inflation, mortgage delinquencies could increase in the coming months as more borrowers see their monthly household budgets stretched further.

“The share of U.S. borrowers who are six months or more late on their mortgage payments fell to a two-year low in August and was less than one-third of the pandemic high recorded in February 2021,” said Molly Boesel, principal economist at CoreLogic. “Furthermore, the foreclosure rate remained near an all-time low, which indicates that borrowers who were moving out of late-stage delinquencies found alternatives to defaulting on their mortgages.”

State and Metro Takeaways:

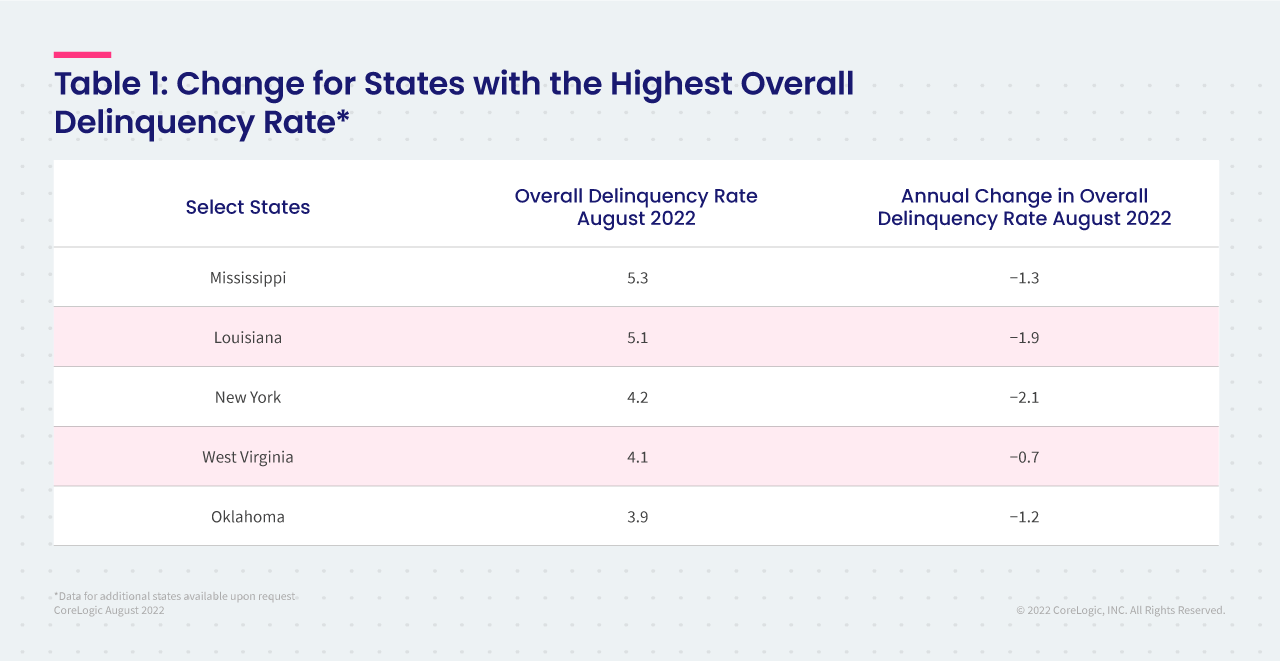

- In August, all states posted annual declines in their overall delinquency rates. The states with the largest declines were Hawaii, Nevada and New York (all down 2.1 percentage points). The remaining states, including the District of Columbia, registered annual delinquency rate drops between 2 percentage points and 0.3 percentage points.

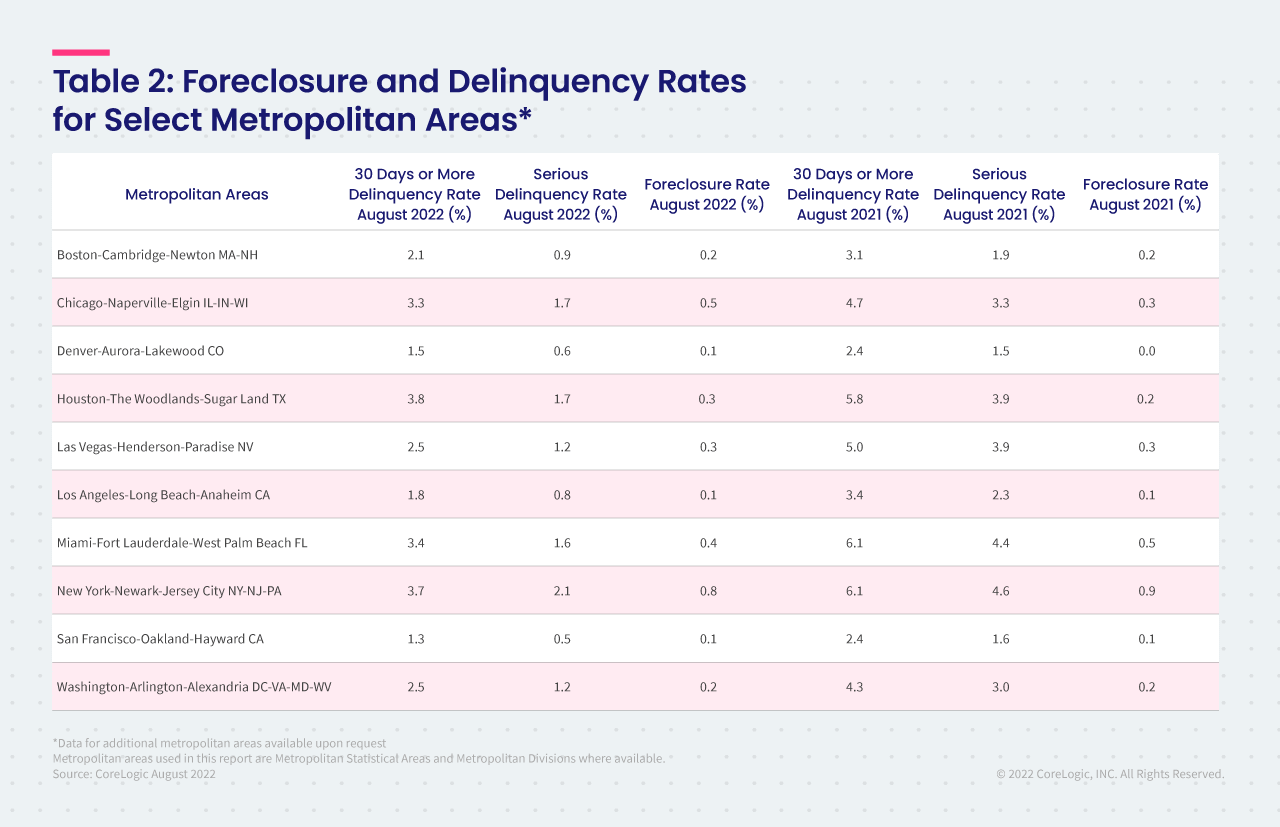

- All but five U.S. metro areas posted at least a small annual decrease in overall delinquency rates, with increases in those metros ranging from 0.1 to 0.4 percentage points.

- All U.S. metro areas posted at least a small annual decrease in serious delinquency rates, with Odessa, Texas (down 4.4 percentage points), Laredo, Texas (down 3.3 percentage points) and Midland, Texas and Kahului-Wailuku-Lahaina, Hawaii (both down 3.2 percentage points) posting the largest decreases.

Methodology

The data in The CoreLogic LPI report represents foreclosure and delinquency activity reported through August 2022. The data in this report accounts for only first liens against a property and does not include secondary liens. The delinquency, transition and foreclosure rates are measured only against homes that have an outstanding mortgage. Homes without mortgage liens are not subject to foreclosure and are, therefore, excluded from the analysis. CoreLogic has approximately 75% coverage of U.S. foreclosure data.