Annual rent price growth has continued to double and even triple in the last several months. This rapid acceleration in rent growth has added to the heightened concerns around inflation for both consumers and federal and local governments. The impact will likely continue to put upward pressure on inflation over the coming year as rent growth is fully reflected in the inflation measure.

“Improvements in the economy and job market have helped push single-family rent growth to record levels,” said Molly Boesel, principal economist at CoreLogic. “However, rapid increases in single-family rents, especially for lower-priced properties, have led to a continued erosion of affordability.”

To gain a detailed view of single-family rental prices, CoreLogic examines four tiers of rental prices. National single-family rent growth across the four tiers, and the year-over-year changes, were as follows:

- Lower-priced (75% or less than the regional median): 10.4%, up from 3.1% in November 2020

- Lower-middle priced (75% to 100% of the regional median): 11.3%, up from 3.3% in November 2020

- Higher-middle priced (100% to 125% of the regional median): 12%, up from 3.8% inNovember 2020

- Higher-priced (125% or more than the regional median): 11.7%, up from 4% in November 2020

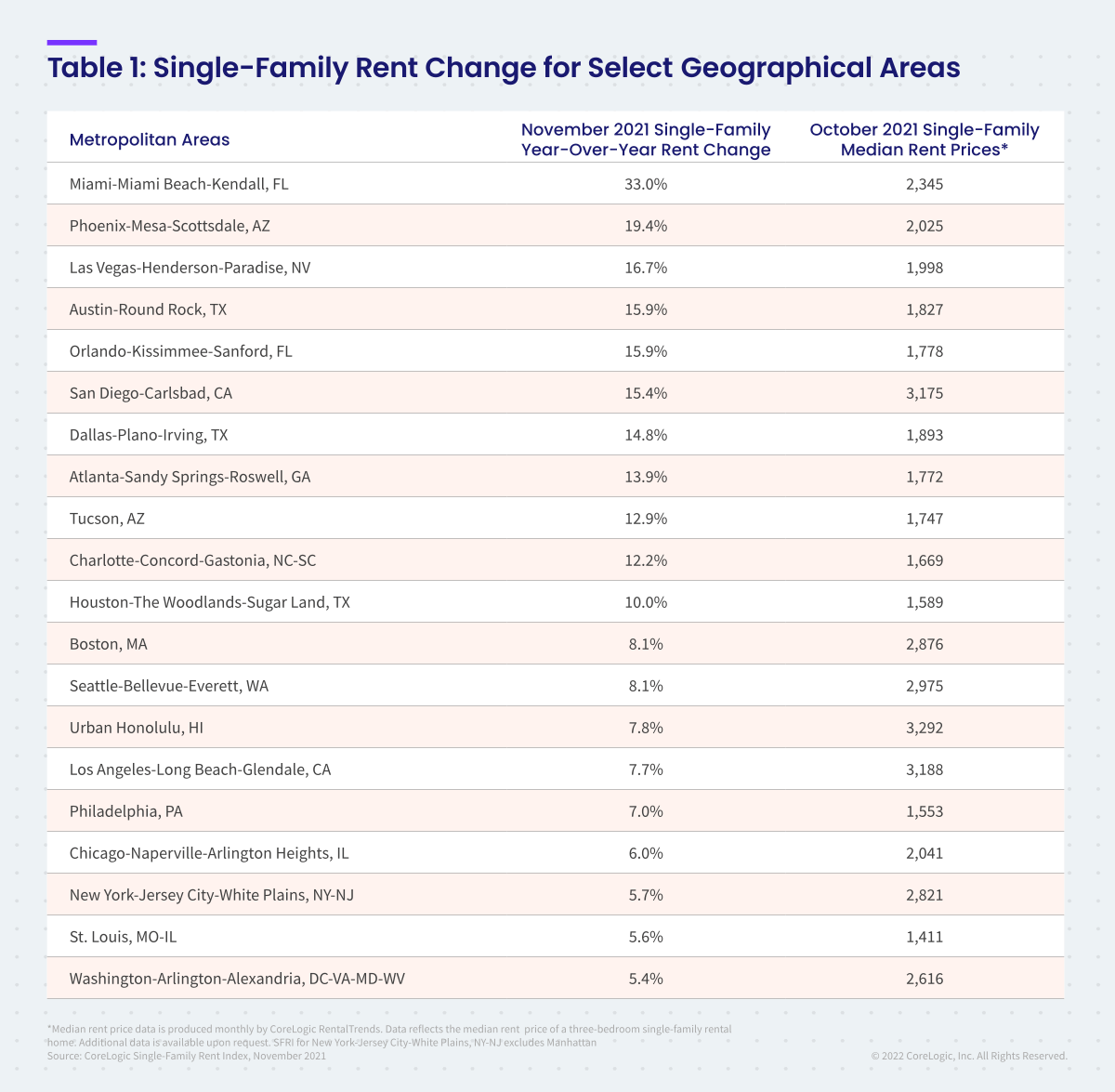

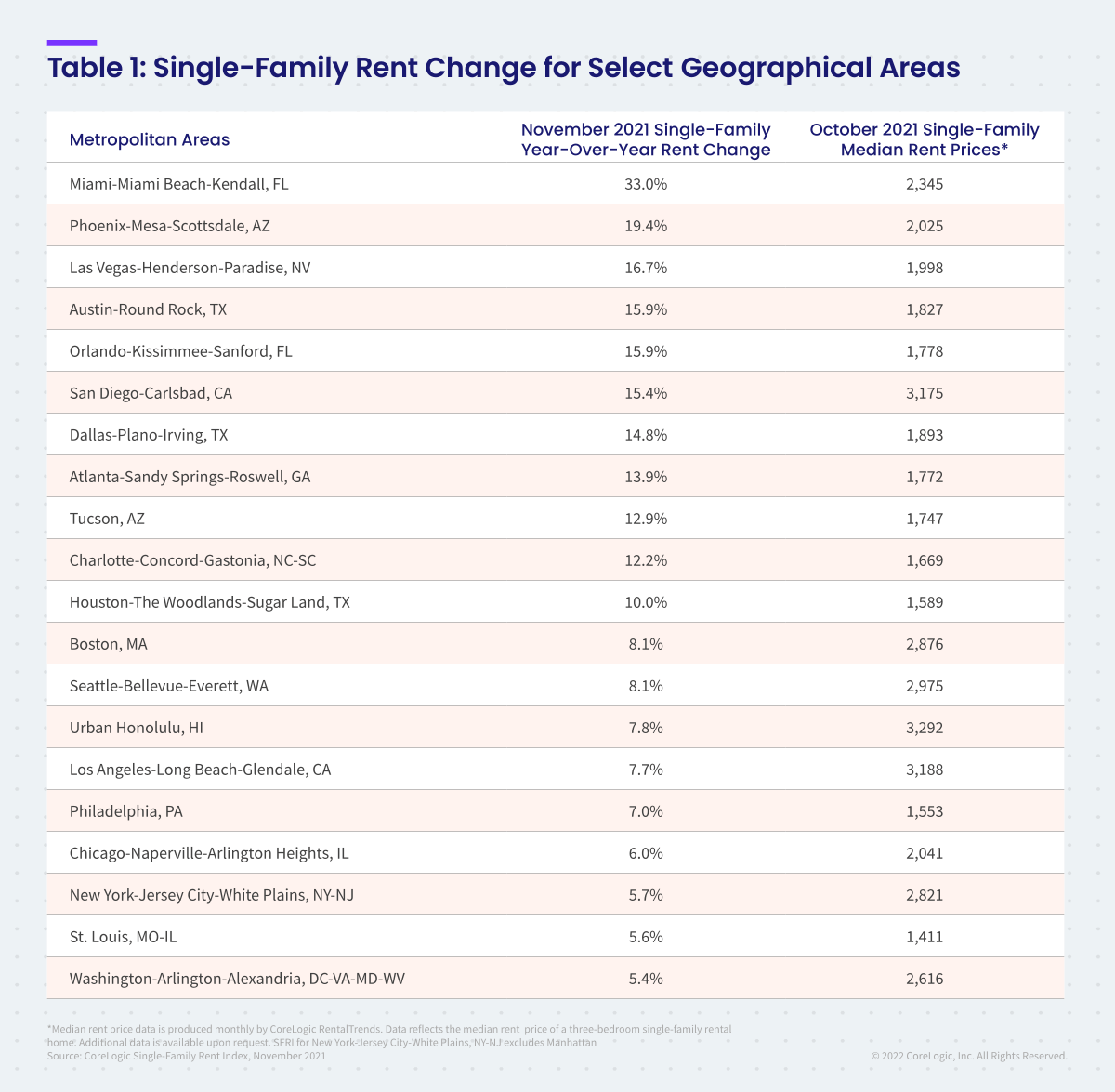

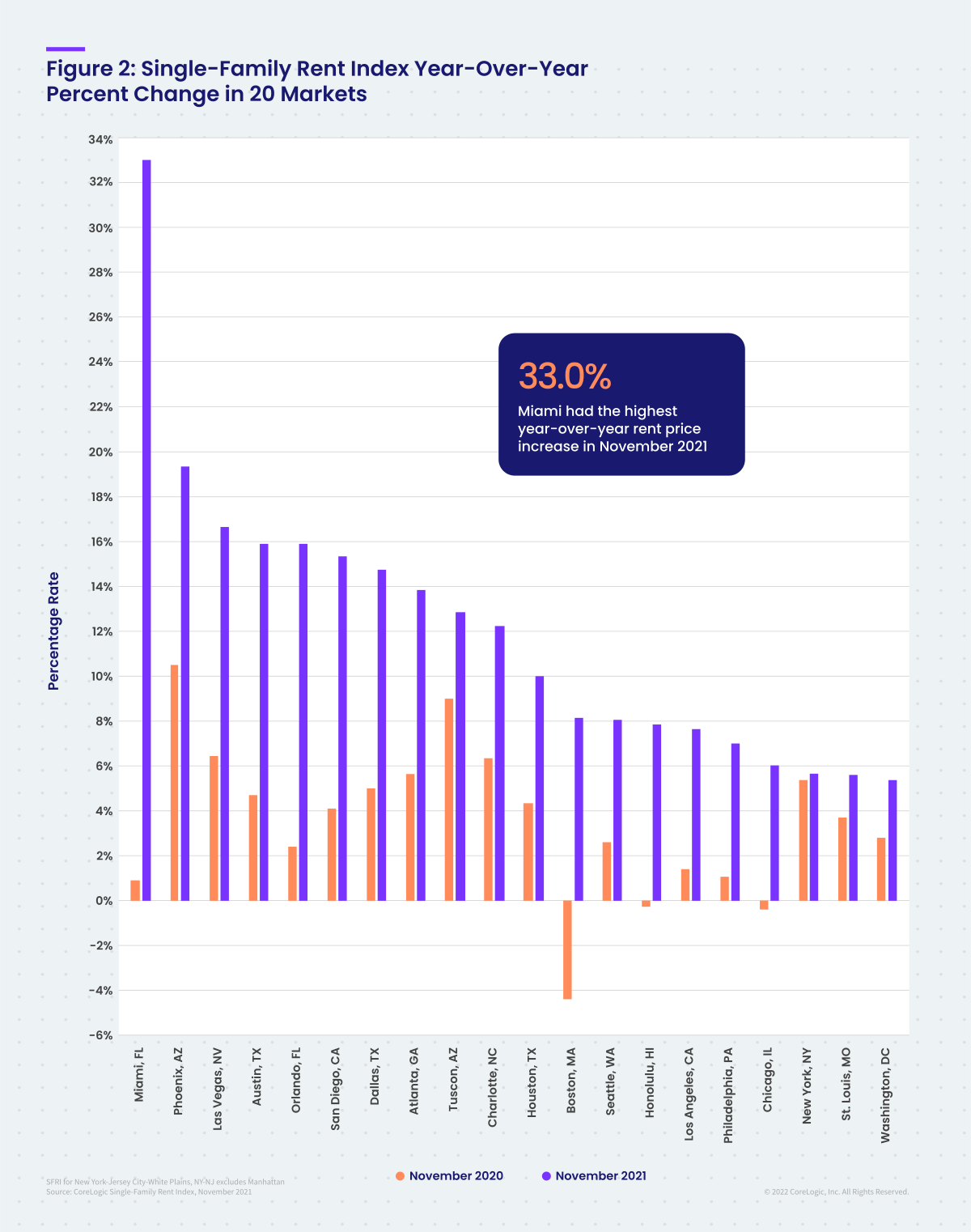

Among the 20 metro areas shown in Table 1, Miami had the highest year-over-year increase in single-family rents in November 2021 at 33%, followed by Phoenix and Las Vegas at 19.4% and 16.7%, respectively. These major metros have continued to experience rapid growth year over year and month over month as unemployment continues to drop and traveling tourism returns. Meanwhile, Washington logged the lowest annual rent price growth at 5.4% in November.

CoreLogic also examines single-family rent growth by property type as shown in Figure 3. Differences in rent growth by property type emerged after the pandemic as renters sought out standalone properties in lower density areas. Notably, rent growth has slowed in the recent month for detached single-family rentals and strengthened for attached single-family rentals.

The next CoreLogic Single-Family Rent Index will be released on February 15, 2022, featuring data for December 2021. For ongoing housing trends and data, visit the CoreLogic Intelligence Blog: www.corelogic.com/intelligence.

Methodology

The single-family rental market accounts for half of the rental housing stock, yet unlike the multifamily market, which has many different sources of rent data, there are minimal quality adjusted single-family rent transaction data. The CoreLogic Single-Family Rent Index (SFRI) serves to fill that void by applying a repeat pairing methodology to single-family rental listing data in the Multiple Listing Service. CoreLogic constructed the SFRI for close to 100 metropolitan areas — including 47 metros with four value tiers — and a national composite index.

The CoreLogic Single-Family Rent Index analyzes data across four price tiers: Lower-priced, which represent rentals with prices 75% or below the regional median; lower-middle, 75% to 100% of the regional median; higher-middle, 100%-125% of the regional median; and higher-priced, 125% or more above the regional median.

Median rent price data is produced monthly by CoreLogic RentalTrends. RentalTrends is built on a database of more than 11 million rental properties (over 75% of all U.S. individual owned rental properties) and covers all 50 states and 17,500 ZIP codes.